A decade ago, most service businesses in Western Europe were small, local, and unscaled. Trusted in their towns, but invisible nationally. Then came a shift. In France, dental clinics began merging, backed by capital [1]. In Germany, it was vets and opticians. In the Netherlands, accountants, staffing agencies, and physiotherapists began consolidating. Each country found its sectors. Each followed a pattern. Fragmented firms became structured platforms.

Belgium moved later. But when consolidation took hold, it delivered. The clearest case is Pia Group, backed by Baltisse, which unified dozens of accounting firms. Hillewaere, Dewaele, and Immo François followed in real estate, scaling regional strength from local roots [2]. None chased hype. They brought clarity, continuity, and repeatability to sectors that lacked all three.

Openthebox, used in this analysis, shows the same pattern reappearing. Many Belgian sectors today resemble accounting a decade ago, with strong margins, recurring revenue, and no urgency to scale. No national brands. Just quiet repetition.

Key Takeaways

- Structure made consolidation work in Belgium

- Many sectors still run small, local, and unscaled

- EV charging and heat pumps are now recurring services

- Financials show low debt, clean margins, and room to grow

- Openthebox shows where structure is forming early

The Belgian Playbook: What Made Consolidation Work

Belgium did not rush into consolidation. It moved deliberately, guided by fundamentals like recurring income, local trust, and operational discipline. The result was not flashy but effective.

From Local Success to Scaled Systems

The Pia Group began like many others: a regional accounting firm quietly serving loyal clients. What changed was not ambition, but structure. Backed by Baltisse, Pia acquired firms that were stable, profitable, yet constrained. These were not distressed assets. They were first-generation businesses, often led by retiring partners, struggling with hiring, regulatory pressure, and rising tech demands.

In just a few years, Pia grew to over 70 offices across Belgium and the Netherlands, employing nearly 2,000 people and generating more than €250 million in revenue. Their 2024 target is €400 million, fuelled by seven new acquisitions and a move into Wallonia. They did not disrupt. They kept local brands, retained partner equity, and made the system run more smoothly. This is consolidation through continuity. Platform-building, the Belgian way.

Hillewaere Insurance took a similar path. Starting in real estate, it shifted to brokerage, where over 5,000 small firms handle most of the market. Many earn less than €1 million annually, struggling to absorb compliance, digitisation, and growth costs.

In just two years, Hillewaere completed eleven acquisitions, scaling to 265 employees and a commission turnover of €34 million. Backed by Rothschild & Co’s Five Arrows, they invested €50 million, with another €100 million committed. Their strategy is to double in size by absorbing firms that are profitable but too lean to grow alone.

The pattern is clear. These are not distressed firms. They are operationally sound, with recurring revenue, low churn, and clean books, but lack the means to evolve. Too small for tech, too lean to diversify, too isolated to negotiate at scale.

In real estate, the playbook shifted slightly. Groups like Dewaele and Immo François kept local identity intact, acquiring agencies with strong roots and forming federated networks. Each office stayed close to its market, while the group offered support where scale created value.

Why These Firms Succeed

What links these cases is not just capital but visibility into succession pressure, margin stability, and strong but overlooked firms. These signals come from records, not headlines. The next wave will rise from sectors that seem too small or too local until they are not.

Where Structure Might Emerge Next

Before turning to specifics, a word on the data. Openthebox draws from filed financials and verified ownership links. It avoids forecasts and scraped estimates. While revenue and net profit are sometimes missing, consistent signals like gross margin, EBITDA, headcount, and group structure remain reliable early indicators.

Some are already clear. In Flanders, cleaning firms have scaled on solid fundamentals. Now, the same traits are emerging in Wallonia. And it is not just traditional sectors. EV charging and heat pumps are shifting from niche offerings to essential infrastructure, with real potential for repeatability and platform growth.

EV Charger Installation: Small Operators Behind a Global Shift

EV charging may appear high-tech, but the ground reality remains fragmented. Hardware comes from global brands, vehicles from multinationals, yet installation and maintenance fall to small, local firms. Most operate independently, without shared systems, scale or integration.

Demand is no longer speculative. It is now structural. Flanders is targeting over 150,000 public chargers by 2030 [3]. What began as upgrades has become critical infrastructure. Each charger needs maintenance, software updates, and replacement cycles. This is not a one-time job. It is a recurring service.

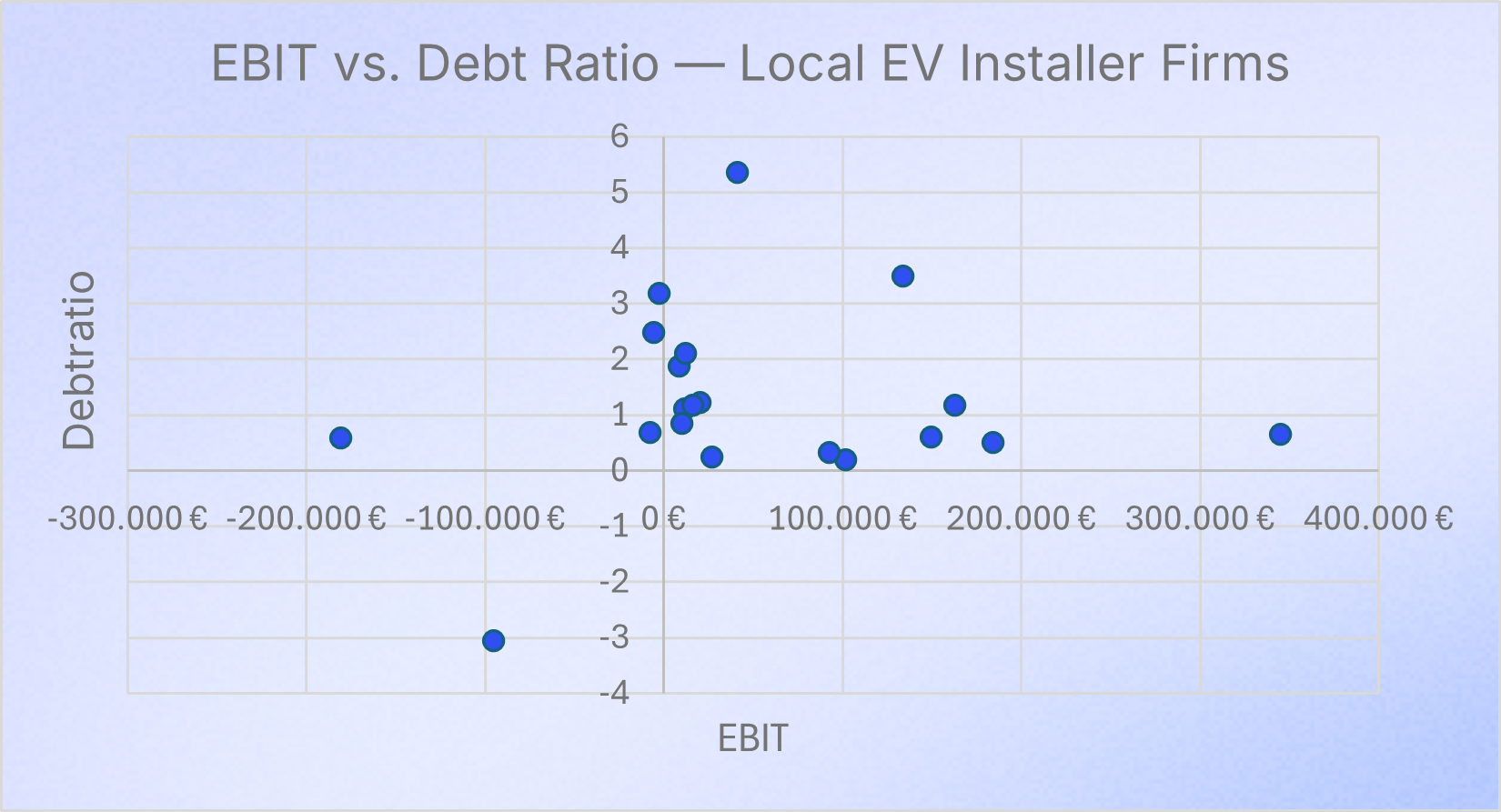

Openthebox data shows that Belgian EV charger installers are small but financially healthy and profitable. Median EBIT is just over €27,000, with some firms exceeding €100,000, showing solid results for companies that often lack scale or growth strategies. Most report low debt ratios, often under 1, and hold positive working capital, indicating sound operations and readiness for expansion. This is not a turnaround story but one of aligning stable, well-run firms into a scalable growth platform.

National EV charging platforms are still emerging, but early signs are promising. De Lijn has committed €24.2 million for up to 900 charging stations to support its zero-emission shift by 2035 [4]. Most firms still operate independently, but with visibility into ownership, margins, and financial strength, the path forward is clear.

Cleaning Sector in Wallonia

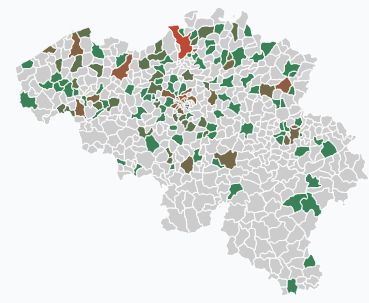

Openthebox maps building and office cleaning as one of Belgium’s most fragmented service sectors. In Wallonia, 74% of providers operate independently. Most are small, family-run businesses with local roots, limited digital presence, and no network ties—forming a dense patchwork of micro-operators, often just kilometres apart.

Map source: Openthebox (2025), based on NACE-coded company activity.

Margin calculations show solid profitability, with EBITDA margins of 10 to 15% common due to recurring contracts and stable costs. In Flanders, some firms have successfully scaled on this model. Wallonia has similar fundamentals, but a different context.

Cultural differences shape strategy. In Wallonia, trust is more personal and hierarchical, unlike the transactional style in Flanders. What works in the north may require a partnership-first model in the south [5].

With no dominant players, low debt, and consistent margins, the sector has all the traits of a platform opportunity. Just one that requires cultural fit as much as financial logic.

Heat Pump Installation: A Sector Built on Regulation and Readiness

The rollout of heat pumps across Belgium is no longer optional. It follows a legislated shift. The EU’s Fit for 55 and REPowerE initiatives are phasing out fossil fuel heating [6]. Belgium is translating this into building codes, subsidies, and efficiency standards. Demand is rising and no longer in question. As with EV charging, it is the small, local installers who do the work, not the manufacturers.

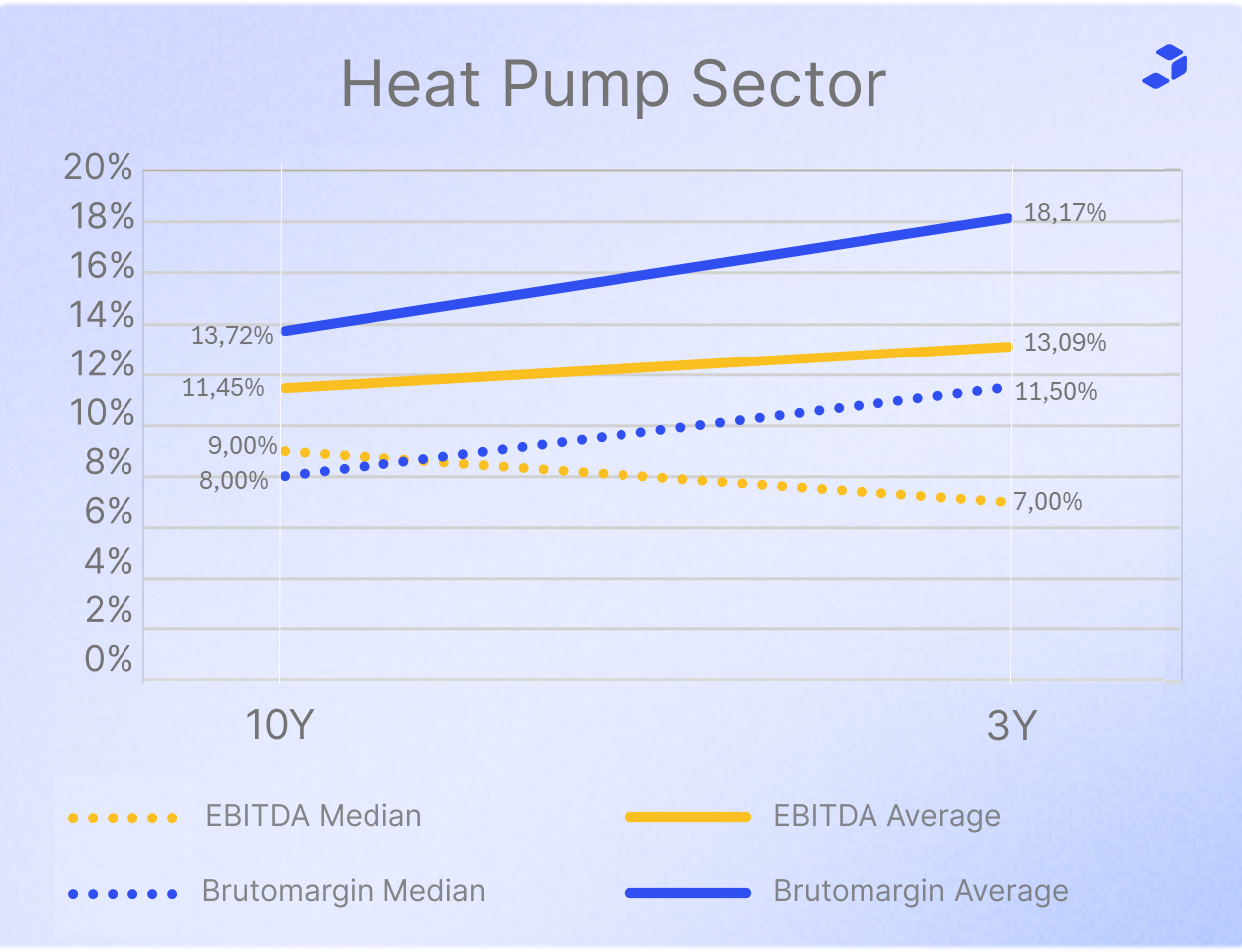

The sector is complex, with systems requiring custom design, integration, and maintenance. Global brands like Daikin and Bosch provide hardware, but local contractors handle delivery, often without scale or affiliation. Openthebox data shows over half the firms with margin trends report multi-year gross margin growth, some above 11.5 percent. As shown below, both gross margin and EBITDA have grown steadily, with a modest acceleration in the last three years compared to the longer ten-year trend.

Based on EBITDA evolution, the median firm has grown at 7 percent annually over three years, with 9 percent over ten years. The average firm shows even stronger momentum, exceeding 13 percent over three years. Most report positive working capital and a typical debt ratio around 1.35, indicating balanced leverage. The fundamentals are solid. What is missing is a shared structure to unlock scale.

Some of these firms already overlap with EV charging, serving similar clients with shared crews. The logic lines up. So does the policy momentum. What is missing is a platform that unifies both. This is a profitable, technical, and policy-led field. It is ready for structure. The question is who will step in first.

Proof, Pattern, Potential

It began in France with dental clinics, in Germany with opticians, and in the Netherlands with accountants and staffing firms. But Belgium has shown it can do more than follow. Groups like Pia and Hillewaere turned quiet, local strength into national scale. Not through disruption, but through clarity, discipline, and timing.

What once depended on instinct and long cycles can now be done differently. With access to filed accounts, ownership records, and verified financial signals, investors can move earlier and with more confidence. Those who use data well will not just find opportunities. They will define what comes next.

Openthebox helps you uncover early consolidation signals

Openthebox helps you spot overlooked consolidation markets by combining ownership intelligence with clean financial signals.

- Group companies beyond NACE codes using keyword filters. Find activity clusters like EV chargers or heat pumps, and see the Belgian market mapped with density heatmaps, ownership overlays, and interactive filters by city, margin, or revenue.

- Assess fragmentation and platform potential using group linkages, independence flags, and regional spread.

- Evaluate financial health with verified metrics like EBITDA, net debt, working capital, and debt ratio, all drawn from filed financials and cleaned for consistent comparison.

Openthebox works across financial sectors like banking and private equity, helping you compare, filter, and move early. Whether sourcing, screening, or designing a strategy, you see what others miss.

Sources

[1] KPMG, The European Dental Market (2017), https://assets.kpmg.com/content/dam/kpmg/xx/pdf/2017/05/euro-dental-market.pdf?utm

[2] De Tijd, multiple articles (2022–2024) on Pia Group, Hillewaere, Dewaele, and Immo François

[3] Vlaamse Overheid, Charging Infrastructure Strategy, https://www.vlaanderen.be/en/authorities/flemish-resilience/expanding-our-charging-infrastructure-is-a-top-priority

[4] Nieuwsblad, De Lijn invests €242 million in EV charging, https://www.nieuwsblad.be/binnenland/de-lijn-bestelt-voor-242-miljoen-euro-laadpalen/42565806.html

[5] CrossCulture Academy, Cultural Differences: Belgium, https://crossculture-academy.com/cultural-differences-belgium/

[6] Council of the European Union, REPowerEU Policy Overview, https://www.consilium.europa.eu/en/policies/repowereu/

.png)

.png)